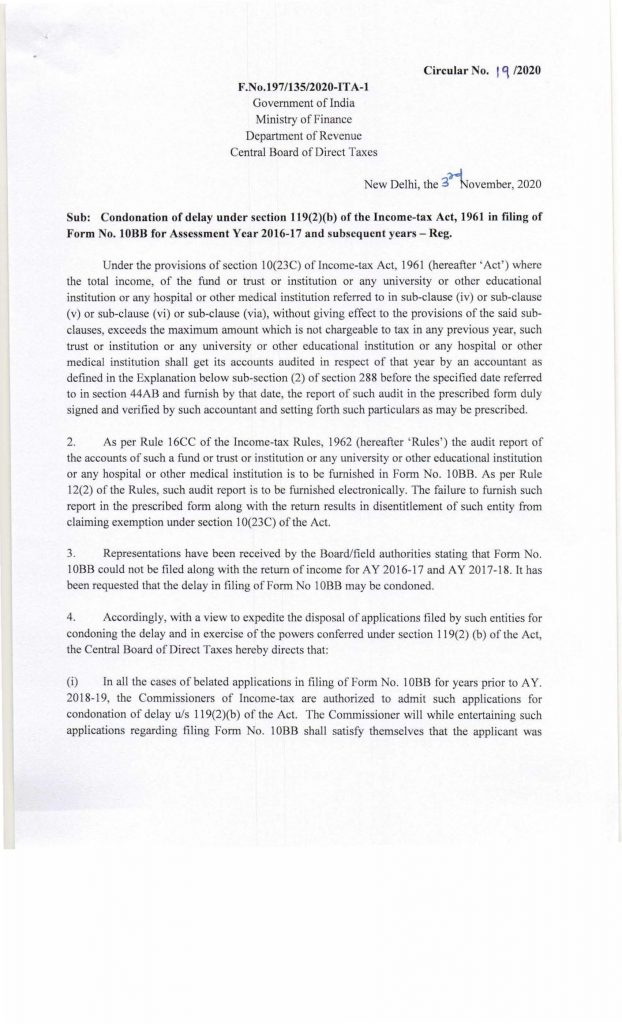

The Central Board of Direct Taxes (CBDT) condoned the delay in filing of the audit report in Form 10BB applicable to entities viz. trusts, institutions, universities and hospitals who claim tax exemption under section 10(23C). CBDT issued Circular No. 19/2020 dated 03-11-2020 under section 119(2)(b) through which the delay in filing of the audit report has been condoned for AY 2016-17 and AY 2017-18. It also empowers the Commissioners of Income Tax to condone the delay of up to 365 days for AY 2018-19 and onwards.

Any funds, trusts, institutions including educational and medical universities or hospitals claiming income tax exemption must get their accounts audited if the total income of that year exceeds the maximum amount not chargeable to tax. To claim such an exemption under section 10(23C), an Audit Report in Form 10BB is required to be filed by such trust or institution. In case of a trust or institution registered under section 11, the prescribed audit report is Form 10B.

The circular states that the Board has received representations from various organizations that they were unable to file their return along with an audit report for AY 2016-17 and AY 2017-18 and to condone the same in order to claim benefit and to avoid litigation. The Board while considering their plea, has issued this circular under section 119(2)(b) on November 3 for condonation of delay for filing Form 10BB.

In this regard, the Board has issued the following directions for providing the relief to such institutes for expediting the process to dispose of such condonation applications –

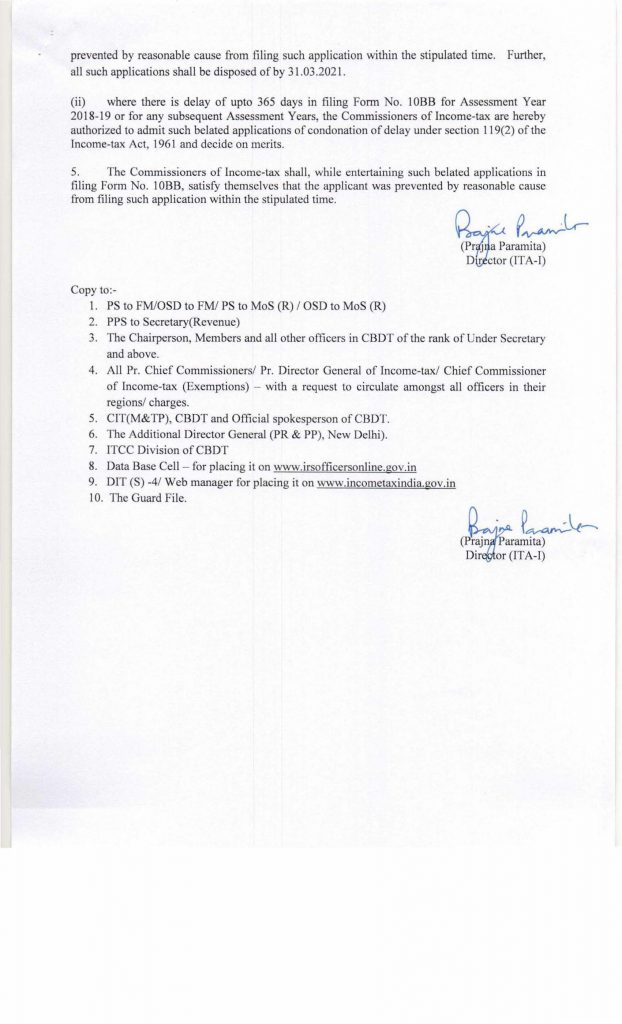

For years prior to AY 2018-19 – The Commissioners of Income Tax shall satisfy themselves that the applicant was prevented by reasonable cause from filing the application within the stipulated time. Further, all such applications shall be disposed of by 31.03.2021.

From AY 2018-19 and onwards – Where the delay is for a period of up to 365 days, the Commissioners of Income Tax are authorized to admit such belated applications of condonation of delay under section 119(2) and decide on merits.

Related Post

Recent Comments